Should You Pay Down Debt or Invest Your Extra Cash? A Canadian Guide for 2026

Should You Pay Down Debt or Invest Your Extra Cash? A Canadian Guide for 2026

📊 TLDR: For most Canadians with an emergency fund, 20+ year horizon, and mortgage under 4%, investing in Canadian dividend ETFs (VDY/CDZ) likely beats debt payoff by $50,000-$80,000 over 25 years — especially in a TFSA or RRSP. BUT: Always pay off credit cards and debt over 7% first.

Imagine this: You've got an extra $20,000 burning a hole in your savings account. You have a mortgage at 3.99% interest and a line of credit (maybe a HELOC) at 4.65%. Both debts feel heavy, but the stock market is calling with potential growth.

What should you do?

Pay off the higher-interest debt first? Chip away at the mortgage for long-term peace? Or invest it all and let compounding work its magic?

This is a classic dilemma many Canadians face in 2026. With prime rates around 4.45% (making variable debt costs moderate) and stock markets offering historical long-term returns in the 7-9% range for diversified portfolios, the math can surprise you.

In this article, we'll break it down simply, look at real numbers, and help you decide what's best for your situation — from mid-income earners to high earners in the top tax brackets. We'll also dive into an often-overlooked factor: inflation, which can make holding debt smarter than you think.

The Problem: Debt Costs vs. Investment Growth

High-interest debt eats your money quietly. Every year you carry it, you're paying interest that could go toward building wealth instead.

But investing carries risk. Stocks can drop 20-50% in bad years (think 2022 or 2008). Debt payments are guaranteed and predictable.

The key question: Does the after-tax return from investing beat the after-tax cost of keeping the debt?

The Debt Priority Ladder (Pay These First!)

Before we dive into the mortgage vs. investing debate, let's establish the hierarchy:

Tier 1 - ALWAYS PAY FIRST:

- Credit cards: 18-22% interest (crushing)

- Payday loans: 300-600% APR (predatory)

- Personal loans: 10-15%

Tier 2 - CASE BY CASE:

- Student loans: 5-6% federal (prime + 1-2%)

- HELOCs/Lines of credit: 4.65-5.5% (variable, tied to prime)

- Car loans: 4-8%

Tier 3 - THE DEBATE ZONE:

- Fixed mortgages: 3-5% (especially under 4%)

- Investment opportunity cost

Rule of thumb: Debt over 7% should almost always be paid off first. Debt under 4%? That's where investing often wins.

Our Three-Way Comparison: $20,000 Over 25 Years

We'll compare three paths for that $20,000 extra cash over a realistic 25-year horizon:

- Pay down the line of credit (4.65% interest saved, tax-free)

- Pay down the mortgage (3.99% interest saved, tax-free)

- Invest in Canadian eligible dividend-paying stocks or ETFs (banks like RY/TD, utilities like Fortis/ENB, or ETFs like VDY or CDZ)

We focus on eligible dividends for better tax efficiency (more on this below).

Why Eligible Dividends Matter in Canada

This is where Canada's tax system becomes your friend.

Eligible dividends come from large Canadian public companies (banks, energy, utilities) that already paid corporate tax. Thanks to the dividend tax credit, they're taxed far more favourably than interest income or employment income.

The Tax Advantage:

In mid marginal brackets (~$100k–$150k taxable income):

- Eligible dividends: 10–25% effective tax

- Capital gains: 12–18% effective tax

- Regular income/interest: 30–40% tax

In highest brackets (over ~$250k):

- Eligible dividends: 36–41% effective tax

- Capital gains: 24–27% effective tax

- Regular income/interest: 48–54% tax

Provincial variation matters: Alberta has lower dividend tax than Quebec or Atlantic provinces. A $10,000 dividend might be taxed at $1,500 in Alberta but $3,000 in Quebec at the same income level.

This makes Canadian dividend investing especially attractive in taxable accounts. But wait — it gets even better in registered accounts...

The Registered Account Game-Changer (TFSA/RRSP)

THIS IS CRITICAL: If you're investing in a TFSA or RRSP, the entire calculation changes.

TFSA (Tax-Free Savings Account):

- NO tax on dividends

- NO tax on capital gains

- NO tax on withdrawals

- 2026 contribution room: $7,000/year (lifetime max ~$95,000 if never contributed)

In a TFSA, that 7-9% return is fully tax-free forever. This dramatically widens the gap between investing and debt payoff.

RRSP (Registered Retirement Savings Plan):

- Tax deduction when you contribute (reduces your income tax now)

- Tax-deferred growth (no annual tax drag)

- Taxed as income when withdrawn (ideally in retirement at lower rates)

- 2026 limit: 18% of prior year income (max ~$31,560)

Example: If you're in the 40% tax bracket and contribute $20,000 to RRSP, you get an $8,000 tax refund. That's like free money to invest or pay debt!

Best strategy for many: Max out TFSA first with your investments, then tackle debt or use RRSP. The tax-free growth in TFSAs is unbeatable for most middle-class Canadians.

Inflation: The Hidden Factor That Makes Debt Cheaper Over Time

We often forget about inflation when crunching debt numbers, but it's a game-changer.

Inflation erodes the purchasing power of money. Today's dollars are worth more than tomorrow's. For debtors, this is a good thing — especially with fixed-rate loans.

How It Works:

If inflation runs at 2% (Bank of Canada's target; December 2025 CPI was 2.4% source: Statistics Canada), you're repaying your debt with "cheaper" dollars over time.

Your 3.99% fixed mortgage has a real interest rate of:

- 3.99% - 2.0% inflation = 1.99% real cost

That's incredibly low! Meanwhile, a variable line of credit (tied to prime ~4.45%) might see rates rise with inflation, keeping its real cost higher.

Fixed vs. Variable: Why It Matters

- Fixed mortgage at 3.99%: Your real cost stays low (~2%) even if inflation rises. You win!

- Variable HELOC at 4.65%: If inflation pushes prime from 4.45% to 5.45%, your HELOC becomes 5.65%. Real cost stays around 2.65-3.65%.

The Wealth-Building Insight:

In moderate inflation (like now), holding low-fixed-rate debt and investing the extra cash can supercharge wealth. Think of it as "good leverage" — real estate investors do this all the time.

If inflation ticks up to 3%, your real mortgage cost could drop to ~1%. But beware: If deflation hits (prices fall), debt feels heavier as money gains value.

Key insight: "At 3.99% fixed with 2% inflation, your real mortgage cost is under 2% — lower than a high-interest savings account!"

The Numbers: $20,000 Over 25 Years (2026 Base Case)

Let's run the math with realistic assumptions:

Assumptions:

- Time horizon: 25 years

- Debt payoff: Interest saved compounds as if reinvested tax-free

- Investing: 4.5% dividend yield (eligible) + 3.5% annual growth = 8% total pre-tax return (historical average for CDZ/VDY)

- Taxes: Annual on dividends (mid bracket ~20% effective); capital gains tax only at end (~26% effective)

- Inflation: 2% (adjusts real values)

- Base case: Mid-income earner (~$100k), investing in taxable account

Scenario 1: Taxable Account (Non-Registered)

| Option | After-Tax Value (25 years) | Real Value (Inflation-Adjusted) | Total Gain |

|---|---|---|---|

| Pay down HELOC (4.65%) | $33,500 | $26,500 | +$13,500 ✓ Guaranteed |

| Pay down Mortgage (3.99%) | $31,500 | $24,500 | +$11,500 |

| Invest: Dividend Portfolio (8% return) | $115,000 | $75,000 | +$95,000 📈 |

Advantage of investing: +$81,500 nominal ($48,500 real) vs. paying HELOC

Scenario 2: TFSA (Tax-Free!)

| Option | After-Tax Value (25 years) | Real Value (Inflation-Adjusted) | Total Gain |

|---|---|---|---|

| Pay down HELOC (4.65%) | $33,500 | $26,500 | +$13,500 |

| Invest in TFSA (8% return, NO TAX) | $136,800 | $89,000 | +$116,800 🚀 |

Advantage of TFSA investing: +$103,300 nominal ($62,500 real) vs. paying HELOC

This is why TFSAs are so powerful. The tax-free compounding adds an extra $20,000+ over 25 years compared to taxable investing.

What If Returns Are Lower? (Sensitivity Analysis)

Conservative case (6% return in TFSA):

- 25-year value: $85,900 ($57,000 real)

- Still beats HELOC payoff by $52,400 ($30,500 real)

Pessimistic case (5% return in TFSA):

- 25-year value: $67,700 ($45,000 real)

- Still beats HELOC payoff by $34,200 ($18,500 real)

You'd need returns below 4.65% annually for debt payoff to win — well below historical averages.

Real-Life Examples: Building Your Dividend Portfolio

Here are some specific Canadian dividend plays popular in 2026:

Individual Blue-Chip Stocks:

Banks:

- Royal Bank (RY): 3.8% yield, rock-solid, 150+ years of dividends

- TD Bank (TD): 4.5% yield, strong US exposure

- Bank of Nova Scotia (BNS): 5.2% yield, higher risk/reward

Utilities (stable, boring, profitable):

- Fortis (FTS): 4.0% yield, 50 years of consecutive dividend increases

- Enbridge (ENB): 6.5% yield, pipeline giant (oil/gas exposure)

Telecom:

- BCE (Bell): 8.5% yield (high debt, but massive payout)

- Telus (T): 6.0% yield, growing wireless business

ETFs for Diversification (Recommended for Most):

VDY (Vanguard FTSE Canadian High Dividend Yield):

- Yield: ~4.5%

- MER: 0.22% (low cost)

- Holdings: Heavy in banks (35%), energy (25%), utilities (15%)

- 10-year return: ~8.2% annualized (source: Vanguard Canada)

CDZ (iShares S&P/TSX Canadian Dividend Aristocrats):

- Yield: ~4.0%

- MER: 0.66%

- Holdings: Companies with 5+ years of rising dividends

- 10-year return: ~9.1% annualized (source: BlackRock)

XDV (iShares Canadian Select Dividend):

- Yield: ~4.2%

- MER: 0.55%

- Similar to VDY but slightly different screening

Pro tip: VDY is cheapest (0.22% MER). For $20,000, that saves you $88/year vs. CDZ. Over 25 years with compounding, that's ~$3,500 more in your pocket.

When to Choose Debt Payoff Instead (The Sleep-at-Night Factor)

Investing isn't free money. Here's when guaranteed debt reduction wins:

Pay Debt First If:

- High interest (>7%): Credit cards, personal loans, some car loans

- Short time horizon (<10 years): Volatility risk too high

- No emergency fund: Build 3-6 months expenses first

- Variable debt in rising rate environment: If prime jumps to 6%, your HELOC becomes 6.65%+

- Psychological peace: Some people sleep better debt-free — that's valid!

- Behavioral risk: If you'd panic-sell in a crash, don't invest

- Deflation risk: Unlikely, but if it happens, debt gets heavier

The Hybrid Approach (Best for Many):

Year 1-2:

- Pay off all debt over 7%

- Build 6-month emergency fund

- Max TFSA contributions ($7,000/year)

Year 3+:

- Continue maxing TFSA with dividend ETFs

- Make extra mortgage payments if it feels good

- Use RRSP if in high tax bracket (get refund, reinvest it)

This balances guaranteed returns with long-term wealth building and psychological comfort.

Provincial Tax Considerations

Your province significantly impacts the math:

| Province | Eligible Dividend Tax (Top Bracket) | Capital Gains Tax (Top Bracket) |

|---|---|---|

| Alberta | 34.3% | 24.0% |

| Ontario | 39.3% | 26.8% |

| Quebec | 40.1% | 26.7% |

| BC | 36.5% | 26.8% |

Takeaway: Albertans get the best deal on dividends. Quebecers pay the most. This can shift returns by 1-2% annually.

The Smith Manoeuvre (Advanced Strategy)

For homeowners comfortable with leverage, the Smith Manoeuvre converts non-deductible mortgage debt into tax-deductible investment debt:

- Make mortgage payment → Increase HELOC room

- Borrow from HELOC → Invest in dividend-paying stocks

- Deduct HELOC interest on taxes (because it's investment debt)

- Use dividends to pay HELOC interest

- Repeat monthly

Result: Your mortgage gets paid off, you build an investment portfolio, AND you get tax deductions.

Caution: This amplifies both gains AND losses. Only for financially sophisticated, risk-tolerant investors with stable income. Market crashes hurt more with leverage.

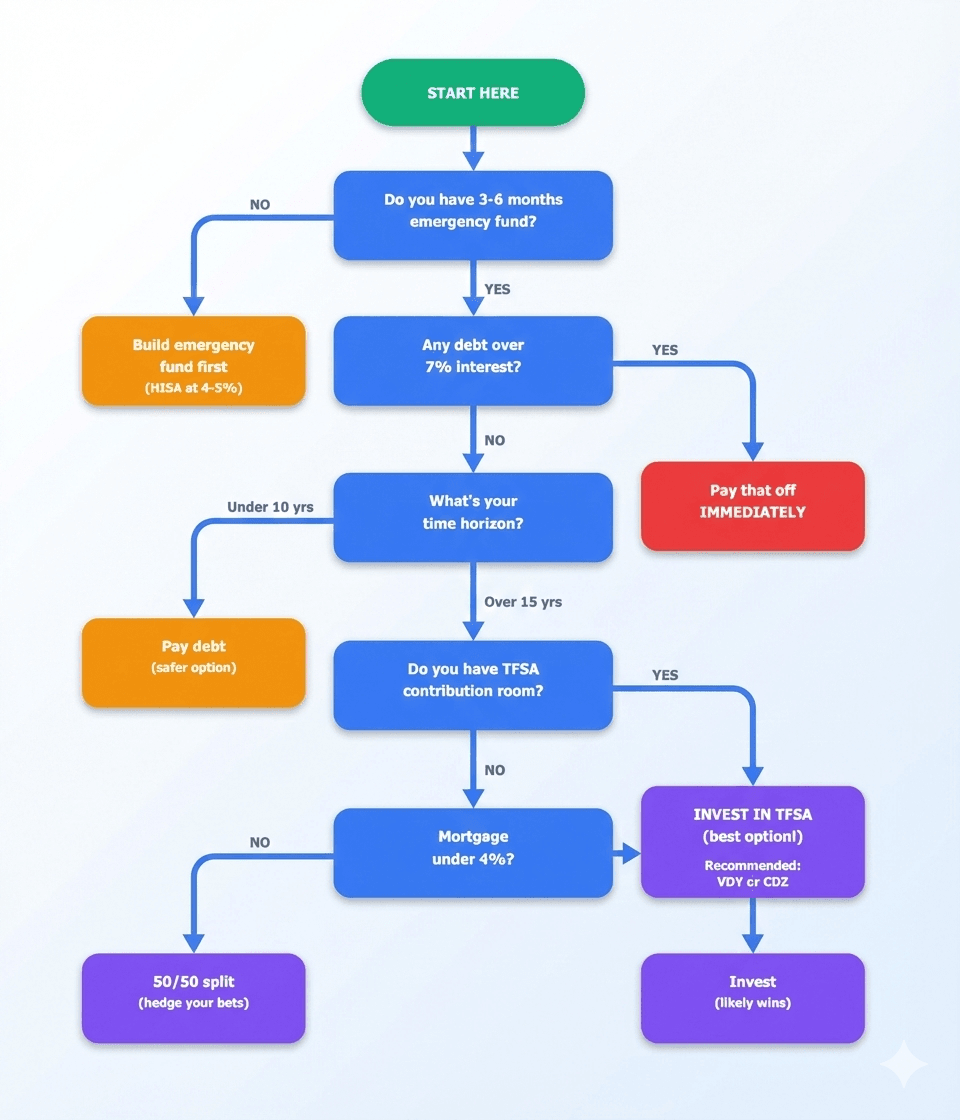

Your Action Plan: A Decision Flowchart

Real Numbers: Case Studies

Case Study 1: Sarah, Age 35, $120k Income (Ontario)

Situation:

- $30,000 extra cash

- Mortgage: $350,000 at 3.74% fixed

- TFSA room: $40,000 available

- No other debt

Best strategy:

- Put $30,000 in TFSA → Buy VDY

- Expected 25-year value: ~$205,000 (tax-free!)

- vs. Mortgage payoff value: ~$49,000

- Difference: $156,000 more from investing

Case Study 2: Mike, Age 50, $180k Income (Alberta)

Situation:

- $50,000 extra cash

- Mortgage: $200,000 at 4.29%

- HELOC: $30,000 at 5.20%

- TFSA maxed, RRSP room: $60,000

Best strategy:

- Pay off HELOC: $30,000 (5.2% guaranteed return)

- Put $20,000 in RRSP → Buy CDZ

- Tax refund (~$9,000) → Invest in taxable or extra mortgage payment

- Reason: HELOC rate higher, but RRSP deduction + low Alberta taxes make investing worthwhile for remainder

Case Study 3: Emma, Age 28, $75k Income (BC)

Situation:

- $15,000 extra cash

- Student loans: $25,000 at 5.95%

- No other debt, renting

- TFSA room: $30,000

Best strategy:

- Keep $10,000 emergency fund

- Use $5,000 → Pay down student loan (6% guaranteed is decent)

- Next year: Focus on maxing TFSA before more debt payoff

- Reason: Young, long horizon, student loan rate is borderline — but building TFSA early captures decades of tax-free growth

Frequently Asked Questions

Q: What if the market crashes right after I invest? A: This is the biggest fear. Historically, markets recover within 3-7 years. If you're investing for 20+ years, crashes are buying opportunities (keep contributing!). If you'd panic-sell, stick with debt payoff.

Q: Should I wait for a market correction to invest? A: Time in market beats timing the market. Studies show lump-sum investing beats dollar-cost averaging 60-70% of the time. If you're nervous, split it: half now, half in 6 months.

Q: Can I deduct mortgage interest on my taxes? A: Not for your primary residence (unlike the US). Only investment properties or Smith Manoeuvre setups allow deductions.

Q: What about GICs? They're at 5% now. A: GICs are great for safety, but: (1) Returns are fully taxable as interest, (2) Lower than historical stock returns, (3) No growth potential. Good for emergency funds or short-term goals, not ideal for 20-year wealth building.

Q: I'm 55 and retiring at 60. What should I do? A: With only 5 years, debt payoff is likely safer. Unless your TFSA/RRSP is already huge and you can ride out volatility in retirement.

Tools and Resources

Free Calculators:

- Morgate Calculator (https://prishanfernando.com/tools/mortgage-calculator)

- Bank of Canada Inflation indicators - Real returns

- Personal Tax Calculator - Provincial dividend tax rates

Fee-Only Financial Planners:

- Advice-Only Planners ($150-400 for one session)

- Look for CFP (Certified Financial Planner) designation

- Avoid commission-based advisors selling products

Further Reading:

- "Millionaire Teacher" by Andrew Hallam - Canadian index investing

- "Beat the Bank" by Larry Bates - Canadian investing simplified

- Canadian Couch Potato blog - ETF portfolios

Final Thoughts: Your Money, Your Choice

Your extra $20,000 isn't just money — it's future freedom.

For most Canadians with low-rate mortgages (<4%), an emergency fund, and a long time horizon, investing in a TFSA with Canadian dividend ETFs creates significantly more wealth than debt payoff — often $50,000-$100,000 more over 25 years.

But there's no shame in choosing the guaranteed return of debt elimination. The "sleep at night" factor is real. Personal finance is personal.

My recommendation:

- Pay off everything over 7% immediately

- Max your TFSA with VDY or CDZ

- Then decide: more RRSP investing or extra mortgage payments?

- Never invest money you'll need in under 7-10 years

Factor in inflation, run your numbers with the tools above, consider your risk tolerance, and maybe chat with a fee-only advisor for $200-300. It's worth it for five-figure decisions.

What would you do with extra cash today — debt or dividends? Share your strategy in the comments!

Disclaimer: This is general information based on 2026 rates and historical returns (not guaranteed). Inflation assumptions based on Bank of Canada's 2% target and Statistics Canada's December 2025 CPI data (2.4%). Tax rules and rates change; consult a professional (CFP, CPA) for your specific situation. This is not personalized financial advice. Past performance doesn't guarantee future results. The author is not a licensed financial advisor.

Sources: Statistics Canada CPI data, Bank of Canada prime rate history, Vanguard Canada VDY factsheet, BlackRock Canada CDZ factsheet, CRA tax rates 2026, provincial tax calculators.

Share this article: Help friends make smarter money decisions! 🚀

Last updated: February 16, 2026

Summary

Discover whether paying down your mortgage, line of credit, or investing in Canadian dividend stocks makes more financial sense. Complete analysis with real numbers, tax implications, and inflation adjustments.